Homestay Financing

Need guidance on homestay financing?

Fill out our guidance request form and we’ll help you find suitable financing options.

Homestay Financing Opportunities in Pakistan I

ntroduction Pakistan’s tourism sector is creating opportunities for families to convert spare rooms and ancestral houses into guest accommodation. Small investments in renovations, safety equipment or business expansion can turn a modest home into a comfortable homestay. This page compiles verified financing options so that aspiring and existing homestay hosts can find suitable ways to fund upgrades, such as building attached washrooms, purchasing furniture and bedding, installing solar back‑up or expanding a small tourism business. Important disclaimer PakHomestay does not provide loans, take applications, guarantee approval or collect repayments. It is an information and facilitation platform. All loan approval, eligibility, mark‑up/profit rates, collateral requirements, tenors and documentation are determined by the relevant bank, microfinance institution or government agency. Please verify the latest terms directly with the offering institution before making any commitment. Financing opportunities for homestay owners Below are key financing options that may be relevant for homestay development. Where exact figures are not publicly available, the applicant should contact the institution for details. NBP Saibaan Home Finance – National Bank of Pakistan (NBP) - Suitable for: Salaried individuals and self‑employed persons who are Pakistani citizens. - Purpose: Purchase of a house/apartment, construction of a house, land purchase plus construction or improvement of an existing home; this can include renovating rooms, adding washrooms or expanding a homestay. - Indicative financing limit: Up to PKR 35 million for purchase or construction; home improvement limits are subject to NBP policy – applicants should confirm directly. - Tenor: Typically 3–20 years for purchase/construction, and 3–15 years for home improvement. - Mark‑up: For salaried customers, one‑year KIBOR + 2%; for self‑employed/business persons, one‑year KIBOR + 3%. - Security/collateral: Mortgage of the property being financed; debt‑to‑equity ratios depend on financing amount (e.g., 70:30 up to PKR 35 million). - Key eligibility: Applicant must be a Pakistani resident national with satisfactory credit history; minimum net income around PKR 35 000 for salaried and PKR 150 000 for self‑employed individuals; maximum debt burden ratio ~50%. - Required documents: Duly filled loan application and product disclosure sheet, CNIC copies, passport photographs, salary slips or proof of income, bank statements, property title documents and proof of employment or business registration. - Where to apply: Visit any NBP branch or the official Saibaan webpage; download the application form and document checklist from the official NBP site. - Important note: Financing terms, limits and documentation can change; applicants must verify current details with NBP before applying. Prime Minister’s Youth Business & Agriculture Loan Scheme (PMYB&ALS) – Government of Pakistan / State Bank of Pakistan - Suitable for: Pakistani citizens aged 21–45 years (18 years for IT/e‑commerce) with entrepreneurial potential. Both men and women can apply individually or jointly. - Purpose: Start‑up or expansion of small businesses, including tourism‑related microenterprises. Up to 65 % of the financing can be used for civil works (renovation or construction), which can help homestay owners upgrade rooms or washrooms. - Financing tiers: * Tier 1: Up to PKR 0.5 million at 0 % mark‑up; unsecured loan with personal guarantee. * Tier 2: Above PKR 0.5 million up to 1.5 million at 5 % mark‑up. * Tier 3: Above PKR 1.5 million up to 7.5 million at 7 % mark‑up. - Tenor: Up to 3 years for Tier 1, up to 8 years for Tiers 2 and 3 (working capital loans have up to 5 years tenure). - Security/collateral: No collateral for Tier 1; personal guarantee for Tier 2; security/collateral for Tier 3 depends on bank policy. - Eligibility: Pakistani citizen with valid CNIC and a viable business plan; loans may require equity contribution of 10 % (Tier 1) or 20 % (Tiers 2 & 3). - Required documents: Application form, CNIC copy, business plan, proof of education/skills if relevant; additional documents may vary by participating bank. - Where to apply: Participating banks (including NBP, Bank of Punjab, Bank of Khyber, etc.); submit applications online via the designated SBP portal or at branches. - Important note: Terms can change; confirm details with participating banks or the SBP website. House Building Finance Corporation (HBFC) – Housing finance schemes - Suitable for: Salaried and self‑employed Pakistanis seeking financing for house purchase, construction, or renovation. - Purpose: Purchase or build a new house; renovate or extend an existing house; potential to fund homestay improvements. - Indicative financing limit: Varies by scheme (e.g., Ghar Sahulat or regular HBFC financing). Applicants must check directly with HBFC for current limits. - Tenor: HBFC typically offers terms from 3 up to 20 years for construction or purchase and shorter terms for renovation. - Mark‑up: Rates are linked to SBP’s refinance rates or KIBOR; consult HBFC for current profit rates. - Security: Mortgage of the financed property. - Eligibility: Pakistani citizens with proof of income; co‑applicant allowed; property must meet HBFC criteria. - Required documents: Loan application, CNIC copies, income proof, bank statements, property documents. Specific checklists are available from HBFC. - Where to apply: HBFC branches or authorized partner banks. - Important note: HBFC schemes may change; confirm details from HBFC’s official website or branches. Islamic home financing (Meezan Easy Home, BankIslami, Faysal Bank and others) - Suitable for: Households seeking Shariah‑compliant financing to buy, build or renovate a home; can be adapted to homestay renovation. - Purpose: Purchase or construction of a house; home renovation or extension (including guest rooms, washrooms, furniture). - Indicative financing limit: Varies by institution (generally from PKR 0.5 million up to PKR 50 million or more). Applicants must confirm limits with the bank. - Tenor: Usually 3–20 years for purchase or construction; 3–10 years for renovation. - Mark‑up: Based on Islamic finance modes such as Diminishing Musharakah; profit rates may be linked to KIBOR or SBP Islamic refinance rates. - Security: Mortgage of the property and sometimes additional collateral; some banks require co‑applicant/guarantor. - Eligibility and documents: Pakistani citizen with regular income, satisfactory credit history, CNIC, property documents, income proof and bank statements. Each bank publishes its own checklist. - Where to apply: Islamic banks such as Meezan Bank, BankIslami, Faysal Bank and Bank Alfalah. Visit branches or apply online. - Important note: Confirm profit rates and eligibility directly from the respective bank. Microfinance options (Akhuwat, NRSP, Kashf Foundation, Khushhali Microfinance Bank, etc.) - Suitable for: Low‑income households, women entrepreneurs and rural families who need small loans for home improvement or microenterprise development. - Purpose: Renovation or construction of rooms, purchase of basic furniture, installation of solar panels, or small tourism‑related businesses such as handicrafts, food and transport. - Indicative financing limit: Generally ranges from PKR 20 000 to PKR 500 000 depending on institution and borrower profile. Exact amounts should be confirmed. - Tenor: Short to medium‑term (6 months to 3 years) with flexible instalments. - Mark‑up: Varies; some institutions offer interest‑free loans (e.g., Akhuwat) while others charge service fees or profit rates linked to microfinance guidelines. - Security: Usually unsecured but may require guarantors; group lending models are common. - Eligibility: Applicant must hold a valid CNIC and meet income thresholds; women‑specific programs may prioritise female applicants or joint liability groups. - Required documents: CNIC copy, proof of residence, business plan or income source; sometimes guarantor CNIC copies and photographs. - Where to apply: Visit the nearest branch of Akhuwat, NRSP Microfinance Bank, Kashf Foundation or Khushhali Microfinance Bank; some also accept online queries. - Important note: Microfinance institutions have limited funds; verify all terms and service charges before applying. SME and rural enterprise financing (Bank of Punjab, Bank Alfalah, Bank of Khyber and others) - Suitable for: Small‑ and medium‑sized enterprises (SMEs), including tourism and hospitality businesses, rural entrepreneurs and women‑led enterprises. - Purpose: Purchase of equipment, working capital, building/renovating guest accommodation, or expanding local tourism services such as transport, food or handicrafts. - Indicative financing limit: From PKR 0.5 million to several million rupees; some schemes are backed by SBP’s refinance programmes. - Tenor: Typically 1–7 years; working capital loans are shorter. - Mark‑up: Profit rates may be subsidised under SBP refinance schemes or determined by each bank; check official sources. - Security: Depending on loan size, banks may require collateral such as property deeds, gold, business assets or third‑party guarantees. - Eligibility: Registered business or sole proprietorship; valid CNIC; business plan and financial statements; sector‑specific conditions (e.g., tourism) may apply. - Required documents: Loan application, CNIC, business registration documents, income/financial statements, bank statements, collateral documents. - Where to apply: Banks such as Bank of Punjab, Bank Alfalah, Bank of Khyber, UBL and HBL; contact SME desks or local branches. - Important note: Terms vary widely; consult the specific bank or the State Bank of Pakistan’s SME Finance Department for current policies. Government and provincial schemes - Wazir‑e‑Azam Apna Ghar Scheme: A federal housing finance programme for low‑income households; details are available through participating banks and the Ministry of Housing. - SMEDA support and SBP refinance schemes: The Small and Medium Enterprises Development Authority (SMEDA) offers advisory services and links to SBP’s refinance facilities for SMEs, including tourism and hospitality sectors. - Provincial tourism & youth loan schemes: Some provinces (e.g., Khyber Pakhtunkhwa) periodically announce loans or grants for tourism entrepreneurs and youth; check the official websites of provincial tourism departments and youth affairs departments for updates. How homestay owners can prepare before applying Before approaching a bank or microfinance institution, homestay owners should prepare basic information about their property, income and planned improvements. This will help lenders assess eligibility and expedite processing. Key items include: - Proof of identity: Copies of CNIC and, if applicable, those of co‑applicants or guarantors. - Proof of residence: Recent utility bill or rent/ownership document. - Property documents: Title deed, mutation or allotment letter; or written permission from the owner if the applicant is a tenant. - Income documents: Salary slips, business income statements, pension slips, remittance records or other evidence of regular income. - Bank statements: Usually 6–12 months for salaried persons and 12–24 months for self‑employed individuals. - Improvement plan: Brief description of the rooms to be renovated, estimated cost, expected number of guests and potential revenue. - Photographs: Clear pictures of the existing property to demonstrate current condition. - Registration or tourism documentation: Any homestay registration, tourism licence or relevant training certificates (if available). - Contact details: Mobile number, e‑mail address, district and village information. Possible uses of financing for homestay development Financing obtained through the above schemes can be utilised for various improvements. Examples include: 1. Room renovation: Repairing walls and floors, painting, adding insulation or improving ventilation. 2. Attached washroom development: Building or upgrading en‑suite bathrooms with proper plumbing, sanitation and fixtures. 3. Furniture and bedding: Purchasing beds, mattresses, wardrobes, tables, chairs and other furnishings appropriate for guests. 4. Solar back‑up or power improvement: Installing solar panels, batteries or UPS systems to ensure reliable electricity. 5. Water supply and sanitation: Setting up water tanks, pumps, filtration units and waste‑management systems. 6. Heating and cooling systems: Installing heaters, geysers, air‑conditioners or fans to maintain comfortable temperatures year‑round. 7. Fire safety equipment: Equipping rooms with smoke detectors, fire extinguishers, first‑aid kits and emergency signage. 8. Kitchen and dining upgrades: Improving kitchens for self‑catering guests or adding dining areas for meals. 9. Internet / Wi‑Fi installation: Setting up broadband or mobile data solutions and routers for guest connectivity. 10. Signage and information: Providing clear front signage, guest information boards and digital check‑in tools. 11. Security improvements: Adding CCTV cameras or locks where appropriate to ensure guest safety. 12. Landscaping and exterior improvements: Beautifying gardens, pathways and outdoor seating areas. 13. Accessibility and hygiene: Making spaces accessible for elderly or differently abled guests and maintaining high hygiene standards. 14. Business expansion: Buying additional equipment or vehicles for tourism‑related services such as guided tours, transport or handicrafts. Need guidance on homestay financing? PakHomestay can guide you in understanding financing options but does not act as a lender. To receive personalised guidance, please share the following details via our enquiry form or contact page: 1. Full name 2. Mobile number / WhatsApp 3. Email address 4. District and village 5. Property location 6. Existing number of rooms and rooms available for homestay 7. Estimated financing requirement 8. Purpose of financing (e.g., renovation, solar installation, furniture) 9. Preferred financing type or bank (if any) 10. Current employment/business/income source 11. Do you own the property? (Yes/No) 12. Message / additional details Click the “Request Financing Guidance” button on this page to submit your information. PakHomestay will review your details and connect you with relevant institutions or provide further advice. Frequently asked questions (FAQs) Does PakHomestay provide loans? No. PakHomestay only provides information and connects homestay owners with banks and microfinance institutions. We do not approve, disburse or recover loans. Can I get financing to renovate my house for homestay use? Yes. Banks such as NBP (Saibaan) and Islamic banks offer home improvement finance that can cover room renovation, washroom construction and furniture. Microfinance institutions and government schemes may also support small‑scale renovations. Can a small business loan be used for tourism or hospitality activity? Small business loans, including the Prime Minister’s Youth Business & Agriculture Loan Scheme, can be used to start or expand tourism businesses. However, borrowers must follow the purpose specified in their application. Are women homestay owners eligible? Yes. Women entrepreneurs are encouraged to apply. Microfinance institutions like Kashf Foundation and Akhuwat offer programmes specifically for women, and PMYB&ALS is open to both genders. Can youth or first‑time entrepreneurs apply? Youth aged 21–45 (18 for IT/e‑commerce) can apply under PMYB&ALS, and many microfinance schemes support first‑time entrepreneurs. Applicants must demonstrate a viable business plan and ability to repay. What documents are usually required? Typically, CNIC copies, proof of income, property documents, bank statements, photographs, loan application form and product disclosure sheet. Microfinance institutions may require guarantor details. Is collateral always required? It depends on the loan type and amount. NBP Saibaan uses property mortgage; PMYB&ALS Tier 1 is unsecured with a personal guarantee. Microfinance loans often do not require collateral. Are Islamic financing options available? Yes. Islamic banks offer Shariah‑compliant home finance and SME finance using Diminishing Musharakah or other modes. Applicants should consult banks like Meezan Bank, BankIslami and Faysal Bank. How do I verify the latest terms? Always check official bank websites, visit branches or call helplines. Terms such as financing limit, mark‑up, tenor and eligibility criteria can change. Can PakHomestay guarantee approval? No. Approval depends on the policies of the lending institution and the applicant’s creditworthiness. What should I prepare before visiting a bank? Prepare a brief improvement plan for your homestay, gather the documents listed in the “How homestay owners can prepare” section, and be ready to discuss your income and repayment capacity.

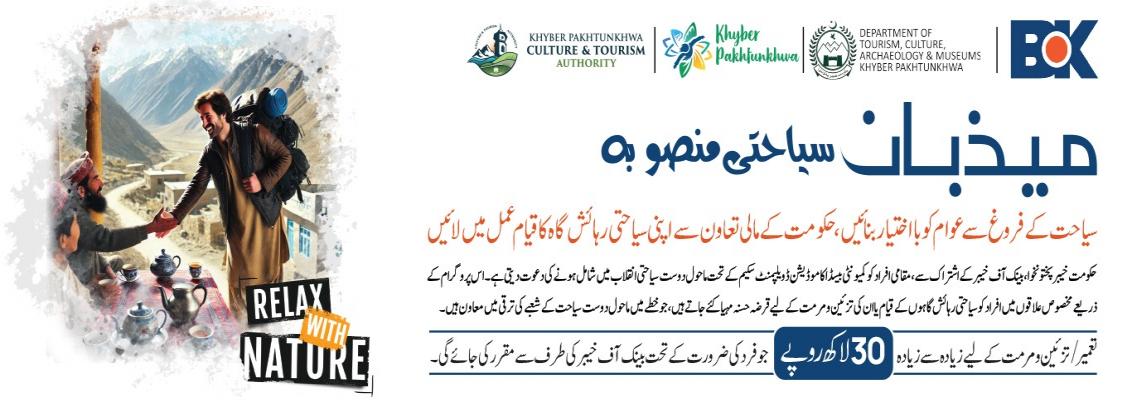

Maizban Tourism Project